Find your IR35 take-home in

60 seconds.

Detailed comparison of tax liabilities for the 2025/26 tax year

If your business was classed as small, the off-payroll working rules do not apply to you for the relevant tax year. Responsibility for IR35 status remains with the contractor’s intermediary. If you were medium or large, you are responsible for assessing IR35 status and meeting compliance obligations.

This page is a free UK IR35 take-home calculator for the 2026/27 tax year, covering both Inside IR35 (PAYE umbrella) and Outside IR35 (limited company) scenarios. Plug in your day rate, working pattern, region, and pension preferences. The calculator estimates net take-home across both routes using HMRC's 2026/27 rates and the Inside IR35 figures match the Worksome Key Information Document format exactly. Built by Worksome, named a Leader in the Everest Group FEMS PEAK Matrix 2026.

How to read your results

Three things to look at, in order. Everything else is detail you can drill into when you want it.

What this calculator actually does

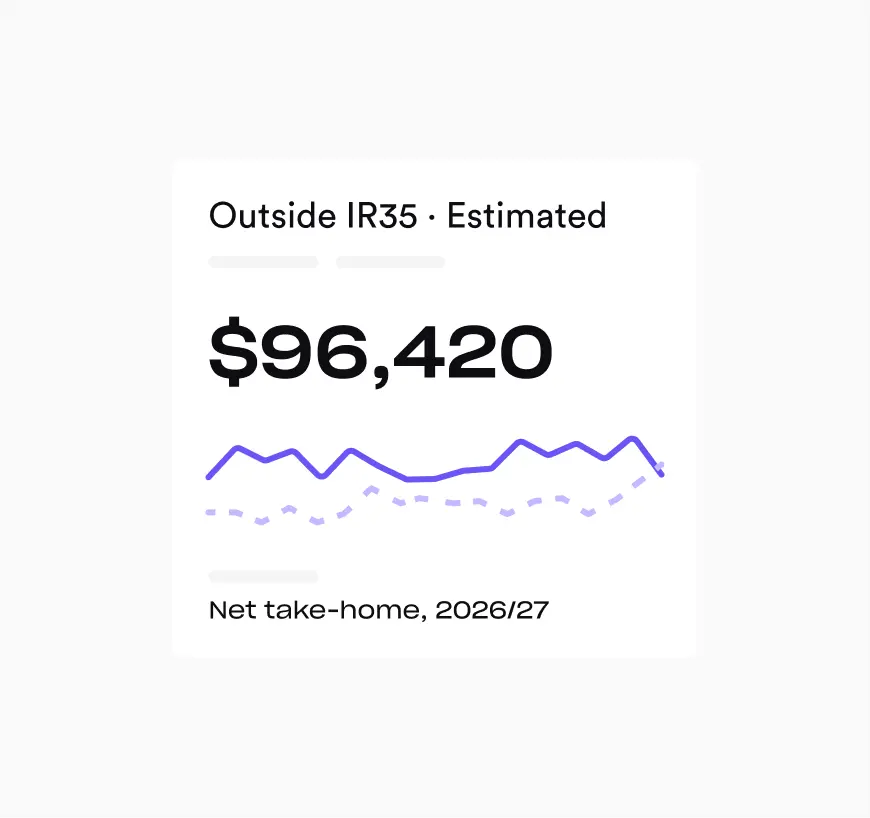

This tool models two scenarios for the 2026/27 UK tax year.Inside IR35:you're paid PAYE through an umbrella as a deemed employee. Outside IR35:you contract through your own limited company and take a small salary plus dividends. Whether you're contracting Inside IR35, Outside IR35, or weighing the two against a permanent salary, this calculator gives you the real take-home for each.

The Inside IR35 figures are formatted exactly like a Worksome Key Information Document — the legal payroll document we issue to every contractor we engage. Open the "Show Inside IR35 KID-format breakdown" panel under the results to see the same line items you'd see on day one of a real Worksome engagement.

Every rate thatchanged this year

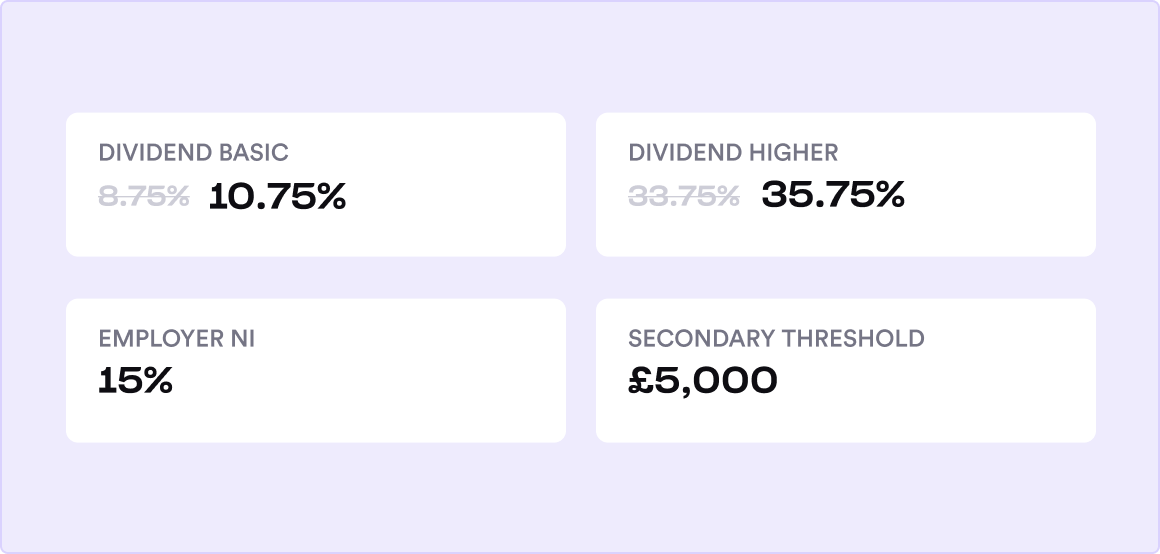

Built on HMRC's actual 2026/27 rates — not last year's, not flat approximations. New dividend tax rates, the 15% Employer NI introduced in April 2025, corporation tax marginal relief between £50k and £250k, widened Scottish bands from January 2026, the 4% EV BIK rate, and Plan 1/2/4/5/Postgraduate student loan thresholds.

decision loginInside IR35 vs Outside IR35

—what's the difference?

—what's the difference?

- PAYE · UmbrellaInside IR35

Deemed employee, taxed at source

HMRC treats you as an employee of the client. Your day rate runs through an umbrella before it reaches you.  PAYE income tax and Employee NI deducted at sourceEmployer NI (15%), Apprenticeship Levy and umbrella fee come off the topHoliday pay rolled in at 10.77% of the booking feeSimpler admin — no accountant, no Self AssessmentLess room to optimise: no dividends, no expense flexibility

PAYE income tax and Employee NI deducted at sourceEmployer NI (15%), Apprenticeship Levy and umbrella fee come off the topHoliday pay rolled in at 10.77% of the booking feeSimpler admin — no accountant, no Self AssessmentLess room to optimise: no dividends, no expense flexibility

Best forEngagements your client has determined as inside, or short-term work where the admin of a Ltd isn't worth it.- Ltd · Salary + DividendsOutside IR35

Employer of RGenuine self-employment viayour Ltdecord

You contract through your own limited company — small salary, the rest as dividends after corporation tax. - Pay 19–25% corporation tax (marginal relief in scope), then dividendsSmall director salary at £5,000 or £12,570 to stay tax-efficientExpense, pension, and partner-dividend optimisations availableFlat Rate VAT surplus + EV BIK at 4% if eligibleYou carry the IR35 compliance risk if HMRC challenges status

Best forLong-term engagements with genuine substitution, control and financial risk — and where the accounting overhead pays for itself.

Inside or Outside IR35? Find out in 5 minutes.

Use the calculator to size the gap. Then confirm your status with our free checker.

Methodology & Sources

Every parameter the calculator uses, every assumption, every rate, every HMRC source. The audit trail for accountants, journalists, and anyone double-checking the maths.